An investment screen to consider - cash boxes with a business attached #3

A retailer

I’ve received a fair few inbounds for FF and I highly appreciate it. There were a few corrections highlighted to me re my initial post, in that

It’s not so easy to simply shutter the biodiesel segment as the chemical business utilizes refined glycerin as a key input which is an output of biodiesel i.e. there are synergies and dependencies between both segments of business.

The chemical facility is operating under capacity especially after losing a big client in P&G a few years ago; the company has pivoted to smaller clients and customized products which has yielded better unit economics, though in the expense of the top-line. Nevertheless, growth remains an issue in this segment and that may be an impediment on how much the chemicals business is worth.

Still, in spite of these “hairs”, the stock is inexpensive and while one might question management’s operational competency - peek their track record - not a single negative FCF year since 2007 and even though the LTM was really bad - FF still generated positive FCF.

Again, a quick back of the envelope math on fair value:

205m of net cash

59 MMgy of flexible feedstock biofuel production capacity

Chevron acquired REG’s 12 biorefineries with nameplate capacity of 505 MMgy for $3.15bn i.e. FF’s biofuel capacity should be worth ~200m minimum (a conservative discount).

There are only two biodiesel producing plants left in Arkansas - FF and Delek Renewables (a small production facility, a fraction of FF’s) - so competition is light in the region which explains FF’s ability to capture positive margins (outside of hedging issues) despite the rough environment

Chemical segment worth 150-200m

In sum, it’s not difficult to envision a stock price >$10 (which FF has historically traded at anyway). There is a weird clause in the 10K that suggests potential dilution should Paul Novelly forces the company to resell all his shares - that may lead to an additional ~6.7m shares floating - i.e. a 15% dilution (against 43.8m shares) → which still pins the stock’s fair value in excess of where it trades today.

Political risks

A key point I’d like to highlight about these cash boxes is to beware of political risks. I’ve shared about Sierra Rutile (SRX.AX) on this blog previously, which had cash covering the entire EV then, locked up offshore in Australia, a huge margin of safety - which should’ve been distributed pronto except time erosion, i.e. deterioration of the rutile environment, the conversion of cash into more inferior forms of liquidity/working capital, topped off with a difficult government, turned the stock to a total dud. Makes me sad thinking about it but just illustrates the importance of keeping an eye out for political risks - those who’ve fished Chinese net-nets would know this too well.

A retail name to discuss

TLYS

Tilly’s doesn’t quite meet the >50% net cash of market cap threshold I stipulated in earlier posts but nevertheless, I find the dynamics quite interesting and thought it worth highlighting. It’s worth noting that there’ve been a fair amount of stocks whereby the company had a lot of net cash but it wasn’t >50% and in many of these instances, the business would trade so cheap net of said cash a position was warranted (even if one argues it’s all “hindsight”) - a prime e.g. being META and in the retail space, AEO or even SIG to name a few. SIG for e.g. has appreciated even as sales tailed off - I vividly recall strolling through Malta in the spring of 2022 pondering about SIG and the stock was in the 60s then vs recent trading price of $105 per share.

Anyway, TLYS - a specialty retailer of apparel, footwear, accessories for children to young adults - currently trades at ~$7.60 per share, sporting a market cap of 228m and projecting 90m of net cash or $3 per share of net cash by end of the quarter, leaving an EV of 138m. The business has sort of tailed off post COVID i.e. 2022 onwards but prior to the pandemic, TLYS earned on average ~40m of OCF and ~15m of CAPEX so around ~25m of FCF. EBITDA ranged around 45-50m so overall, we’re paying around 5x FCF and around 2-3x EBITDA, assuming TLYS returns operations to pre-pandemic levels.

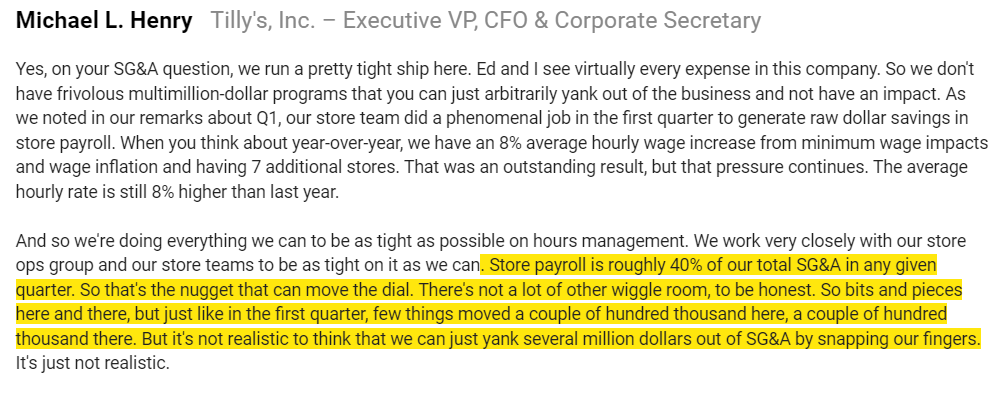

However, the main issue here seems to be that whilst TLYS is able to hold sales (forecasted 625m for 2023 vs 619m of sales pre COVID) level, gross profits have taken a hit due to promotional markdowns especially beginning Q1 23 though it has slowly recovered in sequential quarters i.e. the worst may be behind us in terms of gross margins. However, SG&A has bloated significantly and isn’t too easy to reverse - e.g. you can’t just roll-back wages:

Management is currently undergoing a turnaround strategy, prioritizing more private label, re-strategizing merchandise mix - to buff up gross margins - and has revamped the management team, onboarding a new head of merchandise and Ed Thomas stepping down as CEO. While operational turnaround is just really hard to predict, especially in retail - the value method entails that these tend to be best bought when all is uncertain. With Tilly’s, and unlike other retailers, we have a history of profitability to bank on and the privilege of time given the large cash buffer.

However, what really interested me re this stock is the players at the table. First and foremost, co-founder Hezy Shaked is creeping near 70 years of age (more inclined to sell) and has ownership alignment: owns ~25% of TLYS (via super-voting class B shares) and doesn’t get an exuberant remuneration - he was compensated 420k base pay and 700k in total, inclusive of options, for fy22 (relative to his current ~55m stake). Second, Pleasant Lake Capital owns ~25% of the firm (this is their largest position) and has continued to buy shares in the open market, as recent as last week; other big holders include Shay Capital and Long Focus Capital - makes me wonder if the game plan here is to orchestrate some sort of take private of TLYS - this has been speculated amongst a few for quite some time now but the lack of an outcome does not equate to an impossibility. I must caveat that there isn’t any public record of Pleasant Lake conducting wholesale takeout - the most recent I can find is a faux-offer for Magna Chip in 2015 (the market rightly didn’t believe the offer).

There will also be some difficulties on the financing side of things - with rates at current levels and the operating margin sliver, debt would be difficult to service. The premium would have to be enough for Hezy to agree and I doubt he’s willing to roll his stake into a private levered specialty retailer given his conservative operating style as we shall see in a bit. Nevertheless, despite my contentions, there’s been quite some action in the retail space - a big recent one being CHS’ 2bn revenue operation taken out for 1bn - and the fact that large stakes have been placed on the table makes this very fascinating.

Performance compensation is weighed 25% comparable sales and 75% operating income so the team is incentivized to generate quality revenue growth - “organic” sales growth off current store base with merchandise priced to cover operational expense.

For capital allocation, management is obviously on cash preservation mode but it’s worth noting that prior to 2023, a cumulative $5.70 of dividends beginning 2017, was paid out → ~75% of the current market cap. And this makes sense given that management, with alignment, runs the business conservatively - my guess is management believes ~100m of net cash is the minimum amount to maintain resiliency - so we won’t be seeing a dividend anytime soon but when the business turns and cash build exceeds ~100m, the excess would be guaranteed, distributed back in cold hard cash.

In sum, I think TLYS is quite a fascinating situation though it remains a little head-scratcher here. As usual, open to discussing.