Event #2 - Not another merger arb - Mayne Pharma (MYX), no outs for Cosette

Treading back into the dangerous land of merger arb with sprinkles of legalese, note that this trade is an inherently risky one so due diligence is required. Moreover, I am an owner of shares at prices below the extant trading value.

The basic idea here is that a few months ago, Cosette signed a binding agreement to acquire Mayne Pharma (MYX) for $7.40 per share. As the world went into tailspin, Cosette, predictably got cold feet and is attempting to terminate the deal, invoking the deal’s material adverse clause - which has rarely/never been successfully upheld/adjudicated in the Western/Australian courts. Moreover, Cosette has repeatedly failed to quantify its allegations. The extant stock price implies a less than 40% chance of deal closure in spite of having zero precedence for support.

In any case, this idea came into my radar primarily via one of my favorite merger arb funds (there aren’t that many) from down-under - shoutout to Harvest Lane - who has laid out a succinct article on the case. There was also a well-written article last month on SpecialSituationsInvestments; tweet storms by Puppyeh who has publicly pushed for MYX to be steadfast through hell or high water.

I was quite hesitant on sharing thoughts on this, the now filed chapter-11 Spirit Airlines still sort of tugging at me a little, even after more than a year. Not to mention seeing the nasty blowup at Capri - literally a case about handbags, but what do I know… In any case, arb land is a minefield so caution is warranted.

Nevertheless, this whole case seems rather interesting and worth flagging; it doesn’t carry the same risks as anti-trust where the politics du jour holds huge weight in the final outcome.

There might even be a chance for scooping up more shares potentially in the open later, should there be a nasty trade-down…

Company Background

Mayne Pharma (MYX) is an ASX-listed specialty pharmaceutical company focusing on development, manufacturing, and commercializing of both novel and generic medicine with a particular emphasis on women’s health and dermatology products. MYX was a sleepy stock for years, sort of trading within the A$4 range for a while. The company made some changes within its portfolio, divesting its US-focused generics in late 2022 and pivoting towards women’s health and dermatology.

Our saga begins sometime early Feb whereby MYX’s stock surges on a strong 1H25 financial update, followed by Cosette coming in strong, 10 days after, with a definitive agreement, binding, to acquire MYX for A$7.40 per share.

Cosette, in their own words, is a “U.S.-based, fully integrated pharmaceutical company with a fast-growing portfolio of products in women’s health and dermatology.” As one can see, MYX would fit nicely onto Cosette’s “platform” with multiple synergies to be wrung out as redundancies are cut.

The binding agreement i.e. scheme implementation deed (SID) can be found here.

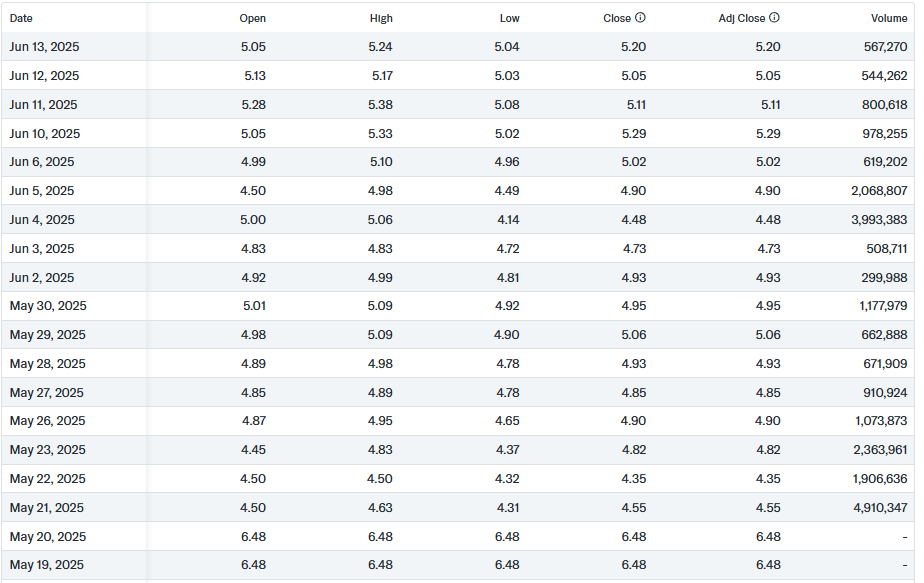

The stock traded at a tight spread for the most part until mid April where things got choppy it sunk below A$7, on news of a litigation by TXMD (11 April). The stock promptly rebounded above 7, and traded a hair above, without much fanfare, even through the earnings update on 22 April. The next big hammer came on 14 May, when the company disclosed that the FDA submitted an Untitled Letter with regards to Nextstellis. The stock took a leg down sinking below A$6 before rebounding above again.

On 17 May, Cosette decided to invoke the MAC clause to renege on the SID. The stock took a leg down on open on 21 May, but has recovered much ground since. Nevertheless, there still remains a sizable arb spread to be captured here.

First and foremost, it’s worth noting that there’s barely any successful invocation of the MAC clause ever, both in US courts and Australian courts. For what it’s worth, the MAC clause has never been successfully upheld by an Australian court, ever.

The most recent upheld MAC case in Western courts, i.e. Delaware in this case, was Akorn v Fresenius - again that was preceded by, quantitatively, a steep decline in Akorn’s profits validated by a sizable extinguishment of its equity value.

A relevant precedent to our case (though in NZ courts, not Australian) would be EQT’s attempted takeout of Metlifecare, of which EQT attempted to use COVID as a MAC to walk from its NZ$1.5b acquisition, which was resisted by MET, and was settled out of court for a ~15%, or NZ$1 price cut (NZ$7 to NZ$6).

MAC analysis

As per the SID, a MAC for this acquisition constitutes: (note the highlighted in bold points)

Any event, occurrence, change, circumstance or matter, whether occurring before, on or after the date of this deed, which has, has had or is (either individually or when aggregated together with any such other events, occurrences, changes, matters or circumstances) reasonably expected to have, the effect of diminishing the consolidated Maintainable EBITDA over a 12-month period of the Mayne Group, taken as a whole, by at least A$10.76 million, other than any event, matter or circumstance:

a) arising solely or predominantly out of the announcement or pendency of the Scheme (including any loss of or adverse change in the relationship of Mayne or any of its subsidiaries with their respective employees, customers, partners, creditors or suppliers as at the date of this deed, including the loss of any contract);

b) required or expressly permitted by this deed;

(c) Fairly Disclosed in the Due Diligence Material (or which ought reasonably to have been expected to arise from a matter, event or circumstance which has been Fairly Disclosed);

(d) Fairly Disclosed in: (i) announcements to the ASX within two years prior to the date of this deed; (ii) a document that would have been returned by a search, in respect of each member of the Mayne Group, of: (A) the public records maintained by ASIC (had the relevant searches been conducted on 17 February 2025); (B) the PPS Register (had the relevant searches been conducted on 17 February 2025); (C) the public records maintained by the High Court of Australia on 27 and 28 November 2024, Federal Court of Australia on 11 February 2025, the Supreme Court of New South Wales on 18 December 2024, the Supreme Court of South Australia on 11 February 2025 and the Supreme Court of Victoria on 2 December 2024; or (D) IP Australia on 17 February 2025; or (iii) a document that would have been returned by any of the searches set out in the Disclosure Letter;

(e) arising from any change in any law, regulation or rule of a Government Agency or accounting standards;

(f) arising from general economic or political conditions or changes in those conditions (including financial market fluctuations, changes in interest rates, commodity prices or foreign currency exchange rates) on or after the date of this deed; or

(g) arising from an act of terrorism, war (whether or not declared), natural disaster, epidemic, pandemic or adverse weather conditions or the like, provided if reasonably practicable Mayne will consult with Cosette in good faith prior to undertaking any action in response to an act of terrorism, war (whether or not declared), natural disaster, epidemic, pandemic or adverse weather conditions or the like that would result in the Mayne Material Adverse Change,

but in the case of paragraphs (e) to (g) above, excluding any event, matter or occurrence which has a disproportionate effect on the Mayne Group relative to other participants in the industry in which the Mayne Group operates.

TLDR, the main crux for a MAC trigger would be a decline in maintainable EBITDA by A$10.76m over a 12-month period. Other considerations which are pertinent to our current zeitgeist - geopolitical tensions, capricious government and rancid policy and war brinksmanship - less a disproportionate impact to MYX, would not be considered eligible for invoking a MAC.

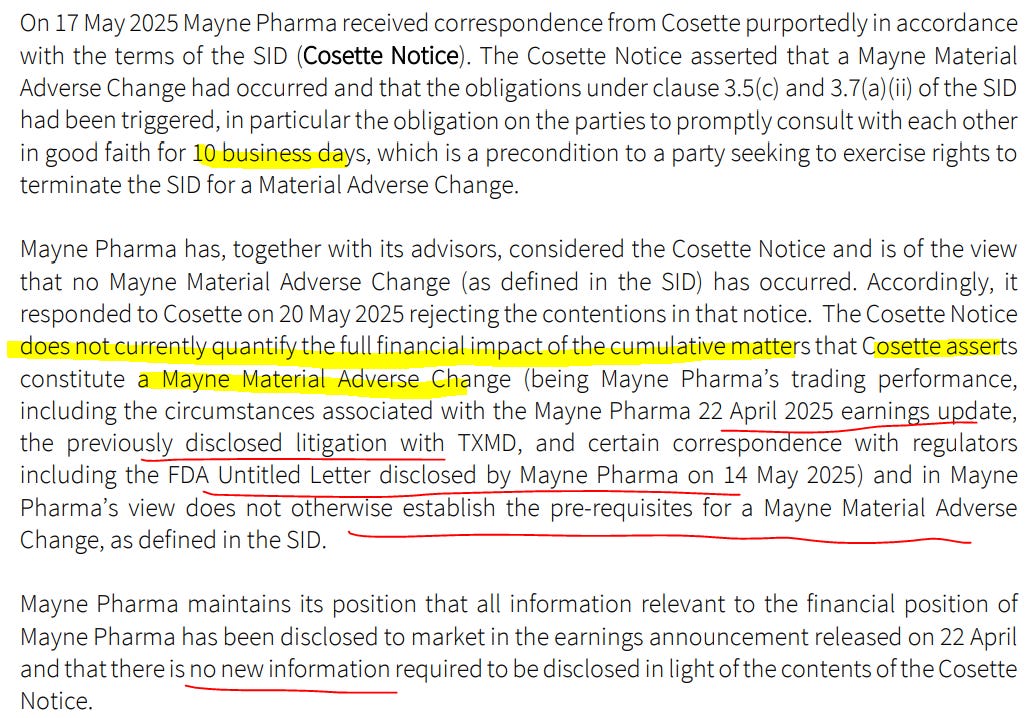

Hence, as per Cosette’s angle on invoking the MAC, Cosette is angling the earnings update on 22 April, the litigation with TXMD and the FDA Untitled letter, putting’em all together to primarily quantify as a breach on maintainable EBITDA, in my view. Moreover, prior to invoking the MAC, the two parties had 10 business days to discuss in good faith the preconditions for such an invocation and as per the PR, Cosette was simply unable to quantify the financial impacts of the matter.

As we shall see, the case is is evidently not strong and without much precedence, if any. Thus, it is likely Cosette is attempting to angle for a price-cut, perhaps analogous to the price-cut obtained at Metlifecare.

Let’s analyze each point of indictment:

i) MYX’s financial performance as per 22 April 2025 earnings update

Perhaps the strongest and the most pertinent of the three indictments, MYX’s financial performance was rather bleak in their recent quarter; MYX saw sales decline 11.3% and a negative A$3.4m decline in EBITDA in Q3 25.

As defined in the SID - maintainable EBITDA excludes restructuring costs, reassessments of deferred liabilities and earn-outs, derivative/swaps/hedging adjustments, legal costs, transaction costs, revenue or profits from non-op activities - essentially adjusted EBITDA.

Perhaps the way Cosette is angling this is by annualizing those losses and voila, we have a breach - annualized A$13.6m EBITDA loss crossing the A$10.76m EBITDA threshold.

However, the CEO reiterated strength through FY25:

Shawn Patrick O’Brien, CEO and Managing Director, Mayne Pharma said “Our nine month performance has seen underlying EBITDA up 116% versus the pcp. The third quarter results were impacted by lower than anticipated volume growth across Women’s Health and Dermatology segments with additional operating expenditures associated with promotional activities for Women’s Health products to build awareness and clinical adoption. Although January and February were challenging, we saw a rebound in our underlying EBITDA for March, which we anticipate continuing through Q4 FY25, with the overall underlying EBITDA in FY25 expected to show growth on FY24.”

In FY25, Mayne Pharma anticipates underlying EBITDA in the range of $47 million to $51 million, representing a 105-123% improvement on FY24, with all three segments expected to deliver a positive contribution.

As per the CEO’s statement, the weak quarter was mainly attributable to declines in January and February which was prior and around the time whence the SID was signed; it is hard to argue that Cossette in their due diligence, were unaware of the the weak two months the company was facing, prior to signing a binding agreement.

Moreover, the firm is guiding to ~A$50m of EBITDA in FY25 which indicates a return to growth in Q4 (cumulative 28.6m of EBITDA through Q3 25) and note, the CEO’s statement was provided on 22 April, with a third of the fourth quarter done with (year ending 31 June). Moreover, even in the 17 May disclosure of Cosette invoking the MAC, MYX maintained its guidance, with one month left to go in the quarter. In other words, less an extreme left-tail disastrous month of June sending the entire quarter into a deep-red bloody mayhem, it is unlikely for Q4 25 to put up a red ink bottom-line.

In other words, there is simply no case to be made with the Q3 25 numbers, even in the chance event that MYX does not hit its FY25 guidance.

ii) Previously disclosed litigation with TXMD

The background here is as follows. Mayne acquired some assets/rights from TXMD resulting in a financial dispute involving primarily, net working capital allowances in relation to the transaction.

The saga is outlined in TXMD’s latest 10Q - pointing to the dispute already surfacing since Feb 2024, culminating in a lawsuit on April 8 2025 (and also verified in the April 11 press release by MYX i.e. “these claims are a series of disputes that have been in discussion between Mayne Pharma and TXMD for some time.”)

The essence of the litigation was due to TXMD alleging that MYX may have misled them in the net working capital adjustment part of the transaction which amounts to ~US$12.1m (~A$18.7m).

Few things to point out, i) the quantum of damages, as per the figures above, appear to be miniscule relative to the size of Mayne’s enterprise (not counting the fact that Mayne has counter-sued TXMD), ii) the disputes were already happening for more than a year (i.e Cosette cannot pull a “colour me surprised” claim) and this lawsuit appears to be a weapon of last resort for TXMD, and lastly, iii) this has no bearing on maintainable EBITDA.

iii) Untitled FDA letter regarding Nextstellis

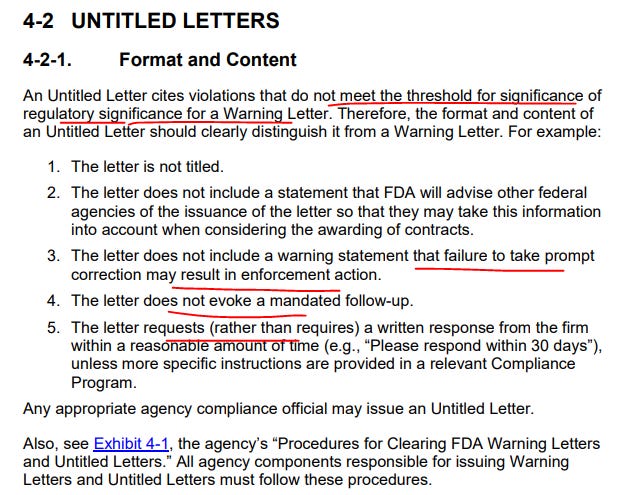

On 14 May, MYX disclosed an “Untitled letter” from the FDA on 28 April, regarding promotional claims used in speaker presentation for Nextstellis. I presume this was the key trigger that Cosette felt it could slam the button on to renege on the SID.

First and foremost, untitled letters are slap-on-the-wrist “parking fines” by the FDA:

Whilst the company did not disclose the letter publicly ASAP, it really is because the whole thing is a nothing burger - parking fine rather than losing one’s license after downing ten shots of tequila and hitting the highway at one-fiddy per hour.

Moreover, the letter and promotional material can all be found on the FDA website. On top of that, MYX stated that it “voluntarily withdrew the speaker presentation referenced in the FDA Untitled letter” and it appears that the FDA had closed out the case shortly after MYX responded to their untitled letter, cite “Based on our evaluation, it appears that you have addressed the violations contained in this Untitled Letter.”

Of course, if MYX simply dismisses the warning and continues to dish out overly promotional materials, perhaps then the FDA will force shut Nextstellis and we will be looking at a sizable EBITDA loss on say A$50m of revenue (80% + gross margins). But again, that’s literally like some left-field event, super retarded and basically, not in the cards here.

Putting it all together

Putting it all together, there is hardly a case to be made for Cosette to wiggle out of this transaction, lest some terrible thing happens to MYX’s business which is basically fair game - that’s what the MAC is for. But as per the current status quo, there is no case to be made.

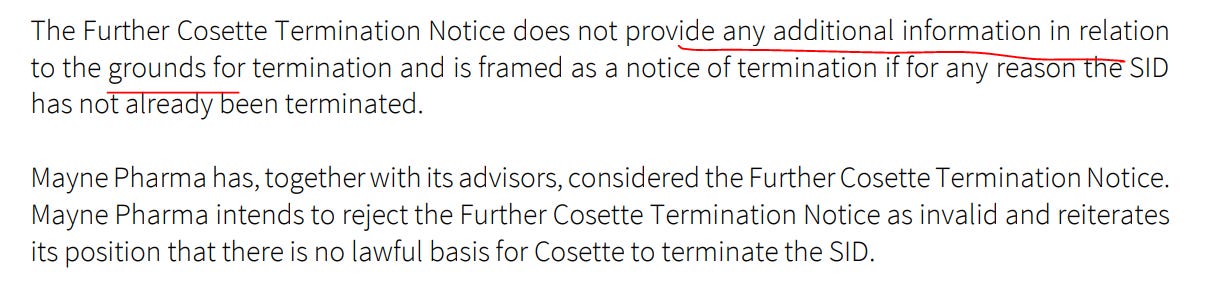

Even the PR on 13 June, whereby Cosette again pushed for a termination, they have not been able to quantify the claims they have made i.e. they really have none. Given that the FDA issue got settled relatively quickly, it appears that Cosette, in a last-minute scramble, on June 14th, accused MYX of false representation in due diligence i.e. (paragraph 15 of Schedule 2) - which actually indemnifies MYX i.e. a carveout for inaccuracies in any forecasts made by MYX management. The onus on determining the reliability of the forecasts is on the acquirer, Cosette, and again, it’s been like 4 months since the deal signing and they could’ve pulled out aeons ago, so this just all seems like one big Hail Mary attempt.

In reality, this is one big game of bluff it seems. One thing I learnt over the last few months is that we live in a big TACO world and so it is very likely that Cosette is TACO-ing this whole thing before coming down a few notches to renegotiate an out-of-court price cut.

Where we are now

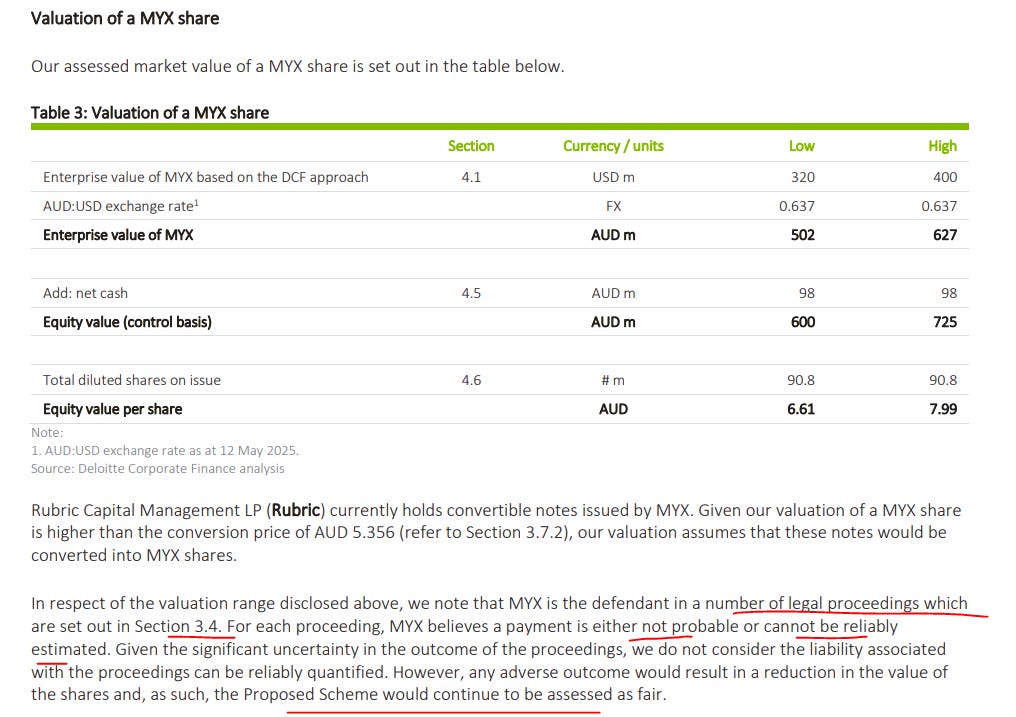

On 15 May, the MYX scheme booklet was published (to inform shareholders for their vote on June 18th) alongside the Independent Expert Report valuing MYX between $6.61 and $7.99 - which also includes acknowledgement of the TXMD litigation, though unquantified given the uncertain nature thereof.

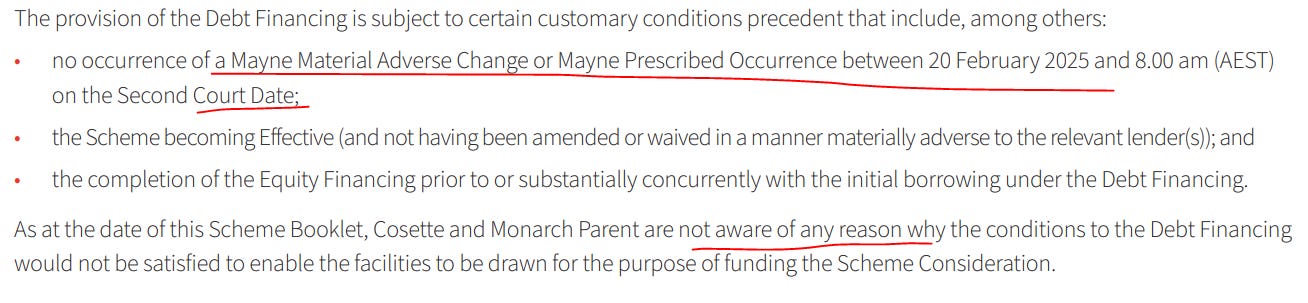

It’s worth highlighting as well that in the same scheme booklet, the debt financing indicates that at the time of publishing, Cosette was not aware of any reasons why the debt financing conditions could not be satisfied. There was nothing materially new publicly between May 15th and 17th (day of termination) for Cosette to suddenly change its mind so timing wise, it’s a huge fumble on Cosette’s part.

Again, this juvenility all makes sense when looking through the lens of Cosette wanting a price recut. This is really sort of the smoking gun, at least to my rather non-expert eyes…

A renegotiated deal, if it were to happen, could likely come at the bottom end the range ~A$6.70, as speculated in various media sources - which would represent a 10% cut give and take.

The break price is a little tricky here and as per the market’s initial knee-jerk reaction on news of Cosette’s termination, shares fell to and closed at a low of A$4.35. Using ~A$4.3 as a potential break price and the recut price as the actual deal price - the market is pricing in a <40% chance of a deal going through, in spite of the fact that the historical odds of a MAC being upheld in the courts of law, specifically in Australia, has never happened before.

On that note, it was also reported that Organon was circling round the firm before Cosette provided the higher, and winning bid. So there is some strategic value involved here that is available not just to Cosette but multiple parties, which should support a stronger break price, in my view.

At ~A$4.3, MYX would be valued at ~11x EBITDA including earn-outs and deferred liabilities, as provisioned in the independent valuation analysis. Excluding the earn-outs, MYX trades at ~6x EBITDA, comparable to Organon, Amneal, to name a few. MYX has sort of traded in the 4 bucks n change range for most of FY24 so I think it’s fair to pin the true break price (not the initial dump in the first hour of the market), around there.

With regards to regulatory clearances, US antitrust has given a green light on the deal and approval from the Foreign Investment Review Board (FIRB) in Australia is pending at the moment. For what it’s worth, Australia made up 10% of revenue in FY24 and will likely be lower in FY25 so obtaining approval on that front; moreover, as we have discussed with MAC, ex a Chinese buyer, there has not been a case where FIRB blocked a US buyer from purchasing a non-strategic Australian asset ever, to my knowledge..

Things to watch out for would be the voting on June 18th. I wouldn’t be too worried about that - ~20-25m shares have changed hand (I’m guessing into sophisticated arb hands like Harvest Lane) since the purported deal termination with other sophisticated holders - Bruce Mathieson with another 5.2m shares and GS with 5.8m shares - so we’ve got around half the total share outstanding covered. Moreover, the offered price by Cosette is at the upper end of the independent valuation range. A price-cut should it happen, would have to happen within the next day or two. Otherwise, assuming a $7.40 set-in-stone price and a deal break of ~$4.30, it would imply a deal chance of <30%.

I will be scooping up more shares on weakness.

Thanks for the write up.

While there is zero precedent for a successful MAC litigation in Australia, it is worth noting that in 2020 two deals were killed by invoking MACs: Carlyle got out of PNC and Madison got out of CML. They just didn't need to go to court.

Having said that, I think both those deals were effected by covid, and the Mayne deal explicitly excludes government action as a cause of a MAC.

It might be that MYX provided Cosette projections with A$60m+ EBITDA in FY25 (not clear, consensus was $58m) and now it's A$50m, so could be close to breaching the MAE threshold. But then, the EBITDA MAC looks a bit loosely worded - which 12 months? decline versus what? - perhaps something to argue about in court.

Another precedent outside of COVID in Australia was Eclipx-McMillan Shakespeare (terminated).

I'm not sure Cosette wants a price cut, though, as a lot of times when it's buyer's remorse or they're spooked by something, they just want out (if they can, of course).