Quick idea: Weight Watchers

Post bk play

“He that lies down with dogs shall rise up with fleas.”

Benjamin Franklin

Quick midnight idea I have to quickly pen before I go to bed. This is one dog-stock, and mind you, not in the cute, fluffy man’s best-friend way but more like the “send to the dog-house” type stock. And despite the ever so wise Ben Franklin admonishing against lying with dogs, chronic dumpster divers, rather than seeking therapy, would rather leave Ben Franklin tossing in his grave…

Caveat, not an expert in post-reorg equity and the likes thereof so let me know if I’ve made mistakes in my analysis.

Anyway, I’ve been eyeing Weight Watchers (WW) for the last few weeks and lo and behold, today was the day they’ve finalized their bankruptcy emergence plan and the stock reacts pretty exuberantly, and of course, I’ve snagged some shares for myself.

*Before moving on, do take caution as this is currently a penny stock (price moves can be wild either way), so none of this is financial advice, do consult a financial advisor and always do your own due diligence.

If you’re wondering, is that the Weight Watchers… the Oprah Winfrey’s Weight Watchers…. yes it is.

Quick Rundown

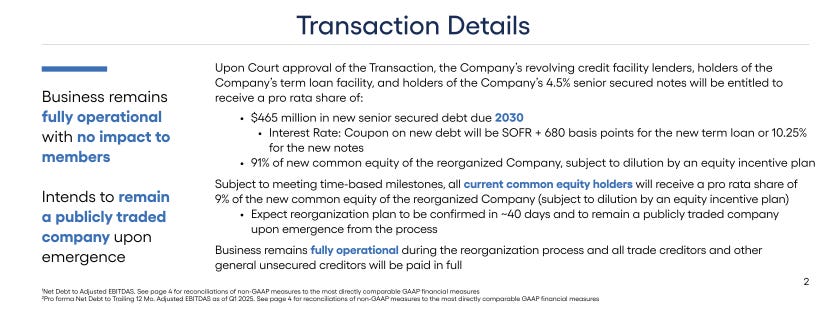

Essentially, Weight Watchers filed bankruptcy last month but differing from the regular one, this was prepackaged/accelerated - something we’re seeing quite a fair bit i.e. VRM, WOLF etc.

The essentials of the bankruptcy plan are encapsulated in this presentation.

To put simply, the bankruptcy restructuring resulted in a balance sheet cleansing of sorts, reducing the amount of debt on the balance sheet via a partial equitization of the debt stack, as well as a refinancing of the residual debt at some cutthroat rate (yikes); and as with prepackaged bankruptcies, original shareholders are not zeroed out, but left with a sliver of the proforma equity, in this case ~9%.

To be fair, WW was not exactly in an imminently distressed state of affairs and hence the bankruptcy was admonished by Bruce Galloway at Galloway Partners, who wrote a letter expressing his frustration, linked here.

Note, Bruce is forecasting EBITDA between $220-250m this year and a fat 15x multiple on that (keep this in mind).

“Weight Watchers is a global brand built over the past 60 years. The Company is at this very time experiencing a strong turnaround, as clearly evidenced by its recent financial performance. Based on market projections, including growth of the Company’s clinical business by 57% and the Company’s strategic shift, as reflected by its recently announced partnership with Eli Lilly, we believe the Company is expected to generate between $220 million and $250 million of EBITDA this year. Applying a conservative multiple of 15 times EBITDA would result in an estimated enterprise value for the Company of approximately $3.5 billion. The Company also has 3.4 million members, which provides a recurring revenue stream, and the membership list, in and of itself, is highly valuable.”

Finally, after waiting a month, WW, a few hours ago, announced the finalization of the bankruptcy and will be completely out of chapter 11 next week.

Pro forma valuation

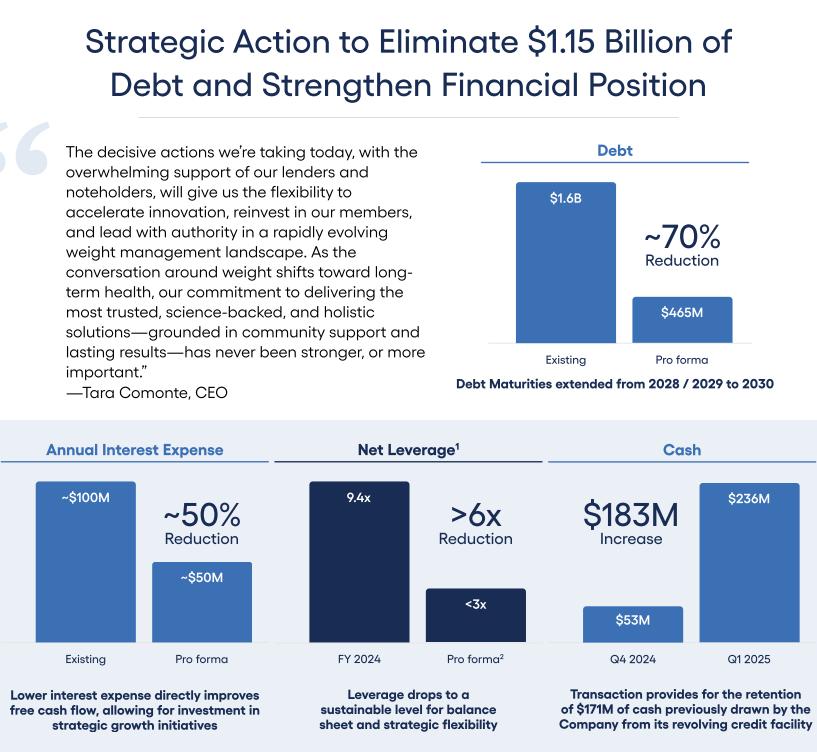

Post bankruptcy, WW would have 465m of debt against 236m of cash with an average annual interest expense of ~50m.

From the old leverage ratio table, prior to restructuring, WW generated $166m of EBITDA in for the LTM ending 1Q25 - SBC is de-minimis and most of the adjustments come from restructuring charges.

Looking, at past financials, FCF (see figure 1) in the LTM was actually positive → 34m of OCF against ~15m of CAPX => 21m of FCF. But again, the operating cash flow numbers don’t tell the full story. As seen in figure 2, WW has been solidly green on operating profits but had all its operating income eaten by expensive interest expense - ~111m in LTM.

WW guided to a 50m reduction in interest expense on the PF equity, so adding that back, with the protection of NOLs, FCF should’ve been ~71m with the new cap structure. Assuming no NOLs, and fully taxed at corporate rate, this should get us to around 60m of LTM FCF.

(Figure 1)

(Figure 2)

With the assumptions laid out above, our proforma equity is trading at a mere 4-5x LTM FCF and around 2-3x LTM EBITDA depending on which set of EBITDA estimates are used.

WW has always had some cyclicality to its numbers but even as recent as 2024, shares were trading somewhere like 10x EBITDA. Without slapping on Galloway’s ebullient valuation targets, even something like 9-10x EBITDA would easily imply a $1.50 stock.

Changes under the hood

Perhaps unbeknownst to most, WW is no longer the traditional consumer business it’s once famously known for. To be fair, this isn’t some weird pyramid scheme that other health-foods companies tend to be. There has been quite some healthy, positive reviews/engagement in various public domains (see YouTube, Reddit), so their legacy business was quite effective at solving what it proposed to solve.

With the rise of GLP-1 drugs, WW has been shuttering its consumer products business whilst also simultaneously rationalizing its cost structure, with a projected $100m of run-rate cost savings, to be wrung out by end of 2025 - taken out of both COGS and SG&A.

But the transformation story doesn’t stop with the pruning of its legacy business.

WW has been pivoting towards its clinical business for a few quarters now which has been growing rapidly at high double digit rates, and this new business prescribes branded and generic weight-loss medication, via partnerships with big pharma (e.g. Eli Lilly) and professional pharmacies (Chequp).

As a result, in FY24, despite declining revenues, gross margins improved significantly, the highest it’s been in a decade (refer back to figure 2).

Moving on to the latest quarter, numbers under the hood for Q1 25 look absolutely fantastic. Not forgetting a quote from the earnings call:

“The profile of this business is one that can be highly cash-generative, especially pre-debt servicing charges, reflective of recurring subscription revenue, high incremental margins and low capital intensity.”

Whilst total revenue remains on the decline, this obscures the record ATH gross margin achieved by the firm, as well as the much superior ARPU numbers resulting from clinical subscription.

In Q1 25, clinical subscription growth grew 47% sequentially, from Q4 24. Note clinical subscription still remains a small part of the business despite the rapid growth - ~130k subscribers at the moment. Again, even on that small fraction, ARPU was uplifted by 4.8% YoY.

YoY, clinical subscribers grew 55.2% and clinical revenue outpaced that, growing 57%.

Putting it all together, Q1 25 was not too shabby a quarter, with the firm hitting a new ATH gross margin, that more or less fell straight through to the bottom line.

Catalyst path

We could quibble what the right EBITDA figure is for this stock (I would love the 15x multiple touted by Galloway) but in any case, the proforma entity trades way too cheaply given the clear inflection in gross margins and ARPU.

With the stigma of the old WW business, as well as the stain of bankruptcy, there is little to like about this stock at the moment, putting it firmly under the radar. The liquidity profile is also rather weak and an up-listing onto the main boards next week, may not provide immediate liquidity given the large overhang of creditors which own ~91% of the equity.

What the mainboard listing should provide however, is some awareness of this 2-3x EBITDA stock with 70% gross margins and a 50%+ burgeoning clinical subscription base.

Also, HIMS, albeit a different business model - vertically-integrated with its own doctors and pharmacy, with a wider variety of drugs covering ED, hair loss, anxiety, GLP-1 - trades at YUGEE significant valuation premium, something like 40x NTM EBITDA and 95x LTM EBITDA.

If WW could even catch a fraction of the multiple, this stock would be multiple times where it is trading right now.

"If WW could even catch a fraction of the multiple, this stock would be multiple times where it is trading right now."

This is the only reason the equity wasn't wiped I believe. The debtholders are hoping to move through bk quickly and draft on the HIMS hype.

The problems for WW's Clinical biz are a) it's a fraction of the size of HIMS and b) the telehealth pill-mill business is very competitive, especially with the pharma manufacturers now going direct.

Sequence/WW's clinical biz is only $120m in annualized revs. HIMS spent $230m on marketing+advertising in the first qtr alone. I think the subscale nature of Sequence/WW's clinical biz could mean it never produces sustainable operating profits.

Then you are left with the core biz that has been in fierce structural decline for years.

I think buying the corp debt was the better play. You were able to get 10% rate debt plus 91% of the equity.

I really like this thesis. Out of the box for sure. A couple quick questions... yesterday the stock spiked 60%. What caused this? Also, won't there be significant technical pressure on the stock as former creditors sell their equity?