Capricorn Energy (CNE:LN) - an orderly wind-down is required

Capricorn Energy (CNE:LN) - an orderly wind-down is required

Quick Background

Capricorn Energy (CNE) is a small-cap British upstream oil and gas company whose assets predominantly consists of cash, contingency rights and a joint-venture in Egypt. CNE’s history is rather fascinating. After winning a long and dramatic tax dispute entanglement with the Indian government which saw the firm pocketing a $1b windfall, approximately half was distributed to shareholders via a common stock tender offer, with the remainder stashed in the bank for growth purposes. Larger firms, wanting to seize on that excess cash balance, made offers for CNE, with seductive “under-the-table” incentives for a rapacious management. Early last year, the old management team attempted to merge CNE in a value destructive deal with Tullow, which was vehemently protested against by key shareholders; end September, management replaced the merger with Tullow, with a merger with NewMed Energy - though a much more sensible deal, still falls short as the best option in creating shareholder value, which in this case would be a distribution of cash and an orderly wind-down of the company. The incessant repugnant deal offers is primarily due to a lack of alignment with shareholders - management owns no stock and stands to gain from the transactions for e.g. the merger with NewMed will leave CNE shareholders with 10% of the proforma entity but provide management with 40% of the board seats, thereby keeping their fat paychecks.

On 19 December, Palliser Capital, one of the larger, more vocal shareholders, demanded an overhaul of management, which took place in late January as the entrenched team waved a white flag and exited the company. The vote for the NewMed merger will take place on 22 Feb though with 40% of shareholders and independent advisors i.e. ISS and Glass Lewis, indicating disapproval, it likely wouldn’t go through.

Without a merger, Palliser and other hedge funds involved are impelling for the, as mentioned, orderly wind-down of operations and concomitantly, an unaffected sum-of-the-parts value that should provide a minimum of 25% upside within the year. Moreover, just by tendering shares at a premium to the extant stock price, affected value could increase by a minimum of 15%, on top of the current unaffected SOTP.

There is no lack of information on this situation given the sheer volume of shareholder protests; this link amalgamates all the key presentations by the activist funds.

Intrinsic Value of CNE

*Note, all FMV estimates are in USD $

Slide 1

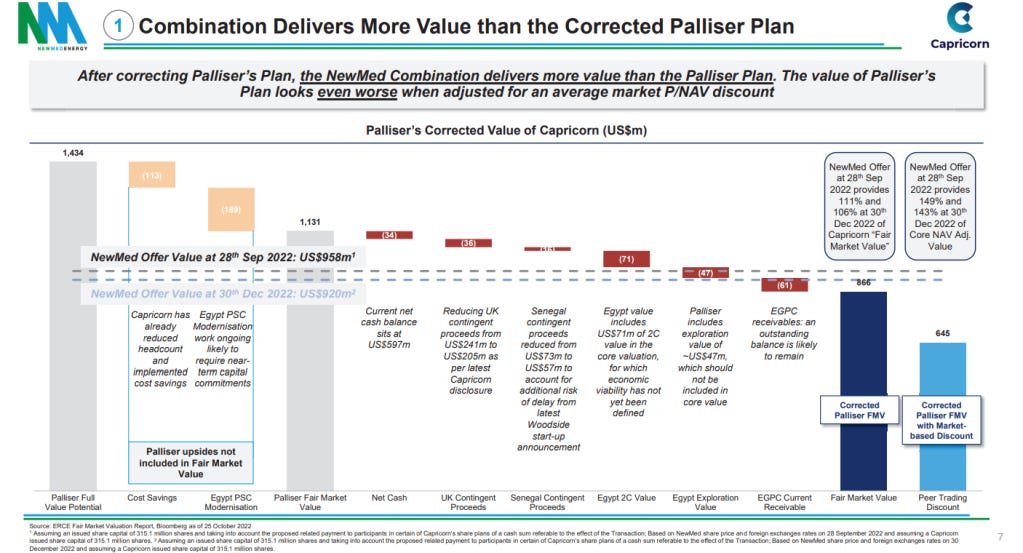

A range of values have been provided by sell-side research and independent consultants; Palliser used the median ERCE valuation in their presentations. Notably, management’s numbers fall far short of external independent estimates, keep this in mind.

Slide 2

Accordingly, 945m of the 1131m FMV are liquid assets - net cash and contingency rights - which equate to 263p of value (assuming Egypt JV is worth zero), outstripping the current stock price.

Another vocal shareholder, Irenic Capital, argues for a 350p NAV, which they claim, could be readily extracted in an orderly liquidation. The exact decimal is not important but the key point here is that it’s not difficult to triangulate >300p of value dormant in CNE.

Management’s Rebuttal

To avoid ignominy, ex-management shot their rebuttal.

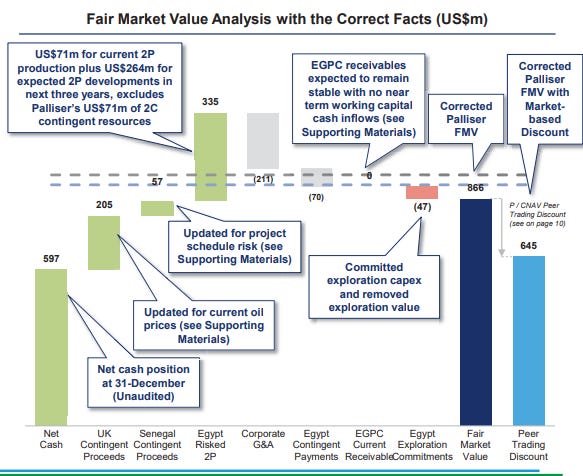

Slide 3

Management makes a few key revisions - adjusting net cash and contingency proceeds down. I will discuss the contingency proceeds in a later section.

In my view, the most ludicrous portion of the slide is the P/NAV discount; zeroing out the Egypt JV, 859m of the 866m of FMV is cash and liquid assets and so imputing an NAV discount on that is simply ridiculous. Management stated elsewhere that distributable cash is 500m tops (Irenic Capital quibbles that 600m through June 2024 is viable), fair. The only issue is that if CNE is truly worth 645m only, then net of the 500m of distributable cash, management is only imputing 145m for all the contingency rights and Egypt JV. Clearly, this is nonsensical and a scare tactic employed to deceive unsophisticated shareholders.

Even assuming 866m of FMV is accurate, that leads to 230p of stock price value which is a 5% downside from the current trading price of 244p.

Egypt Assets

Let’s attempt to estimate the Egypt Assets.

The Egypt JV was disposed by Shell in March 2021 with Cheiron purchasing 50% and CNE taking the other half, at a net purchase price of $323m USD and a book value of $330m.

CNE has indicated that it was a competitive bidding process and it probably took place somewhere in late 2020 and early 2021. So while one may argue that CNE suffered the winners’ curse, this is offset by the fact that Brent Prices were lower ($60 vs $80+ today) and oil and gas assets were trading for much cheaper. In addition, Net WI production was forecasted to decline in 2022 before rebounding in 2023 and so an acquirer would be buying into a production decline.

Management in order to suppress FMV, applied some punitive discounts to the Egypt assets.

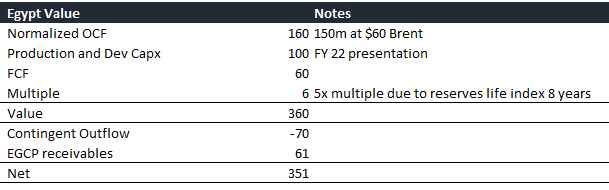

i) Referring back to Slide 3, management did not include $71m (refer to Slide 4) of risked value of 2C contingent resources in their $335m estimate, despite, stating, at the time of acquisition, “near term growth opportunities” from this resource base.

Slide 4

ii) Attributed zero value to EGPC receivables (JV partner doesn’t report the same issues) and applied a punition for exploration CAPEX (arguable if this should equate to some value or not so, fair).

Hence, from slide 4, we could argue that ever since the deal, ex-management has either imprudently incinerated 180m of value or is once again finding ways and means to suppress FMV. Ironically, in the call discussing the combination with NewMed, ex management gassed up the Egypt assets with descriptions such as “crown jewel”, “fast to market, rapid payback, very high IRR”.

Ignoring ERCE’s (slide 2) 400+m estimate for a moment, let’s attempt some quick back-of-the-envelope valuation.

Asset Value

Purchase price was $323m in 2021 and net book value was $334m as of H1 22, due to depletions. Add a 20% Brent premium to the purchase price and keep P/B at 1x and we can triangulate between 335 to 380m of fair value.

Earnings Value

The Egypt JV generated 105m of gross profit, 53m of EBIT and 50m of OCF in H1 22, depressed by working capital issues.

EV/EBIT

Capitalizing 100m of annualized EBIT and slap on a 3-4x multiple and we get 300-400m of value.

FCF multiple

In the FY21 call, ex management estimated a sustainable 150m of OCF per year at $60 Brent Prices. If Brent stays >$70 and say that yields $160m of OCF, subtract 100m of guided maintenance CAPEX for production, development (100m), that nets out to 60m of FCF which a 5-6x multiple (accounting for the poor reserve life balance of 8 years - 90m reserves against 33k bpd production) would equate to 300-360m of value. Deduct the contingent outflows to Shell, add back the receivables and that should chip off 9m of value.

Rather than using a multiple of FCF, we could use the NPV method; running the numbers out for 8 years, say 60m FCF per year at a 10% discount rate, that gets you an NPV of 320m; if you raise the initial years FCF to 70m (higher strip prices currently and lower maintenance capex), you can really bump the NPV up to 340m easy.

Do note that there is a lot of sensitivity to the OCF and CAPEX numbers. For OCF, 2/3 of Egypt production is gas which is sold to the government at a fixed price while the remaining 1/3 is liquids which is indexed to oil prices. However, this is offset by the fact that the $100m of development CAPEX is mainly catch-up CAPEX after years of negligence by Shell (previous owner). In the FY20 call, management reassured that normalized CAPEX would be lower.

Regardless, it’s fair to say that we could take a midpoint value of say 350m, which is still a >10% haircut to ERCE’s estimates.

Contingency Rights Discussion

Just to dive a little more into the non-cash assets. The contingent earnouts (CVR) are claims on a stream of cash flows which CNE earns from assets sold and is usually part of divestment transactions. For e.g. the UK CVR (larger % of total CVR claim) is attributed to the sale of North Sea assets to Waldorf in November 2021 and is the NPV of the uncapped cash interest CNI receives over the subsequent 4 years. The Senegal CVR is from the sale of Sangomar assets to Woodside in December 2020 and is slightly different in that it is a lump-sum payment to be received upon first oil production.

Both CVRs require average annual Brent prices to remain in excess of $52/bbl up till 2025 so the earn-outs are currently deep in-the-money (ITM), which brings me to my next point – why can’t CNE just sell these CVRs (to a third party or to the issuers themselves) at a slight discount (on top of PV-10) and convert them all to cold hard cash. Industry dynamics would most likely support Brent prices and keep the CVRs deep ITM but even so, the futures market is liquid and though there is some backwardation, prices can easily be hedged, by an institutional buyer with ISDA certification. (I go into more detail in the appendix)

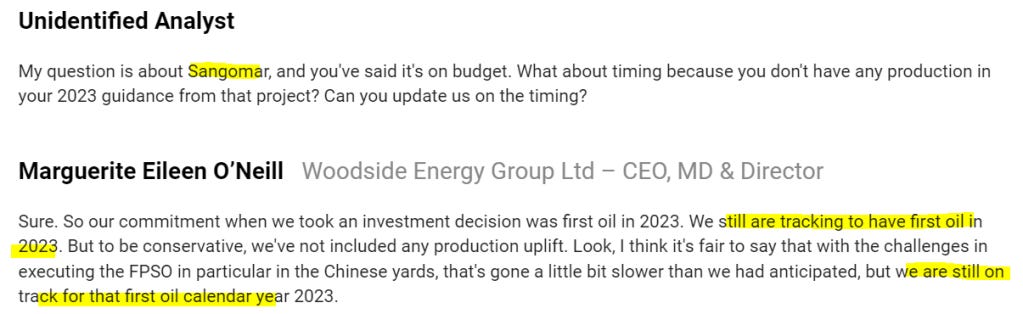

The Woodside earnout is particularly interesting in that if first oil is produced in 2023, then CNE receives 100m and if in 2024, then 50m. Obviously CNE’s ex management downplayed the value of the CVR by marking it at a mere 57m when Woodside has explicitly stated two months ago that they are still on track to having first oil in 2023 (see image below). Moreover, Woodside is a huge company (48b USD mkt cap) so they’re not going to play monkey and defer production, just to avoid paying out an extra 50m.

1/12/22 Investor Briefing

SOTP

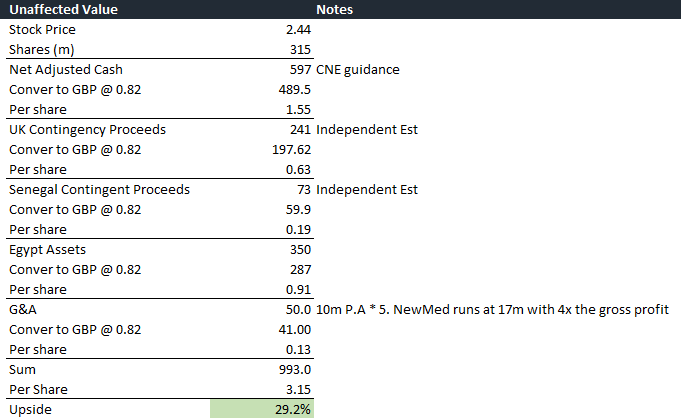

Unaffected Value

Assuming ex-management’s net cash estimates are true, utilizing the independent estimates for CVR value, pinning the Egypt JV at mid-point 350m and subtracting a right-sized G&A, we can pencil north of 25% upside easy on an SOTP basis.

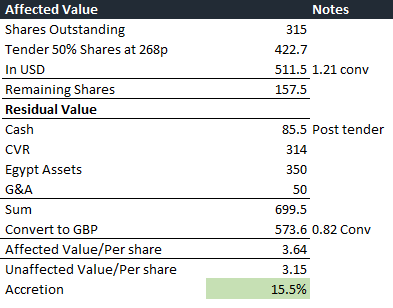

Affected Value

In the hypothetical scenario that CNE conducts a tender offer for 50% of shares at a 10% premium to the extant stock price (244p at time of writing), this would be immediately accretive to per share value by >15%, that is on top of the >25% unaffected value upside.

Do note that no value is accounted for CNE’s exploration licenses in UK, Israel, Mexico, Suriname and Mauritania - certainly these would have value to a strategic major.

Final Pointers

The Egypt JV assets are low cost-curve assets, albeit with an average reserve and resource life index of 12 years (8 + 4), extremely capital intensive and some may argue that it would be difficult to divest in a wind-down scenario. However, if the initial bidding was indeed competitive, then why would that be any different if CNE puts the JV up for sale today?

For example, CNE managed to offload their minority interest in the declining North Sea assets to Waldorf at >1x book value (cash upfront + CVR) back in early 2021, way before the whole “oil super-cycle” theme emerged. Moreover, after the 2022 windfall, most oil majors have less precarious capital structures and are able to pony up for assets. Let’s also not forget that Shell had neglected these Egypt assets for a number of years and so the immediate buyers, CNE and Cheiron in this case, had to bear the upfront additional CAPEX to backfill the economic costs of Shell’s underinvestment. But a portion of that has been completed now and that should definitely augment valuations.

The stock price is also another baffling piece of the puzzle. Despite good news of management changes, and a potential for “significant distribution of cash in excess of operating requirements“, the stock price barely budged. This is a little like Carlyle, they brought in ex-GS Harvey Schwartz, slapped on a comp package tied to stock price appreciation and the market greeted that with a big fat yawn – $CG is now down 7% in the last 5 days. On the other hand, in Germany, Bayer announced an outsider CEO and boom, stock jumps 7% in a day, though some of the gains have been returned; the point is, why the muted reaction at CNE when the value proposition is so clear coupled with activist funds involved? Maybe the market is skeptical of UK corporate governance and this is another show-not-tell case which is very justified, especially for those actively involved in UK markets.

Appendix

*Note I am no derivatives expert so this is just my 2c, based on studying past transactions.

Let’s use the CVR from Waldorf as an example.

The CVR from Waldorf is an uncapped contingent consideration payable to CNE when Brent trades above US $52/bbl on average in the five years 2021 to 2025. The sensitivity to Brent prices is quite astounding: $100m of cash generation at $60 Brent, $175m at $70 Brent and $240m at $80 Brent. Concomitantly, rather than subjecting the value of the CVR to the whims of the oil gods, an institutional owner of the CVR could implement a vanilla put spread - buying a put at the prevailing Brent prices and and selling a put at $52/bbl - essentially hedging the entire move down to the floor price of the CVR.

If said owner were to apply exotic options, they could structure it in such a way whereby the put spread kicks in only when Brent touches a certain price (say $80), for a customizable period of time; this easily lower the cost of the entire spread given the owner of said spread doesn’t capture the immediate downside exposure from the current price to the “kick in” price

In any case, with an options spread implemented, the only risks would be isolated with the counterparty, i.e. Waldorf/Woodside - will they honor the contingent payments (which they will because it’s a small piece of the pie for them) and will they proceed with production/development as planned.

Disclosure: Long CNE