Further thoughts on Silk Laser (SLA.AX) (Updated 1/6/2023)

**Update at bottom of article

Quite clearly my initial prognostication of a direct bidding war was flat out wrong - I underestimated the underlying game theory and Wes’ acquisition discipline. As of this morning, Wes has indicated that it will not exercise matching rights i.e. to match EC’s superior offer; accordingly, Wes’ process deed will be terminated and EC will be granted due diligence.

Lets back-track a little with regards to the contents of the process deed. This is a competitive protection mechanism of sorts for Wes, in that they were granted exclusive due diligence, no shop, no talk and a unanimous director recommendation (a transaction prerequisite). Should a competing offer arise, Wes would be granted all relevant information about this competing bidder and would be given 5 business days to match or top the bid; the competing bidder will have no access to private due diligence throughout.

In this instance, Wes has decided not to exercise matching rights and thus, forfeits the process deed, granting EC permission to conduct due diligence as they wish.

At A$ 3.12, I find the r/r rather fascinating and have added more to my position. In my mind at the moment, there are two event paths that could take place from here.

Before getting into the potential payoff states, fundamentally, this stock trades at ~8x EBITDA and is floating below its Dec 2020 listing price. Of course, the market was way more exuberant then and one could argue that they are overearning at the moment. However, comps such as API’s Clearskincare, generated 28% EBITDA margins pre-Covid in 2018; yes, a higher margin treatment mix (laser) compared to SLA’s injectables though this should be offset by SLA’s franchise business which enjoys full revenue to cash flow conversion.

The two states are as follows:

EC walks.

Both parties have proposed non-binding offers and I discuss the credibility of the offers in the previous piece.

Nevertheless, the market seems to be implying a spurious bid to a certain extent given the ~7% spread from EC’s $3.35 take out price. Worth noting that risk free rates are higher now so spreads would not be as tight as before.

Say EC walks, having never been a serious bidder in the first place, or maybe realizing, upon doing DD, that the acquisition isn’t worth it - what synergies are there to be had for a wholly HK business? One could point to expansionary expertise and franchise potential, maybe, but those aren’t easily realized.

But in the event that EC changes its mind, Wes is already sitting on ~9% of SLA and remains the sole acquirer, thus the $3.15 deal likely goes through and apart from stale money, one doesn’t lose from here.

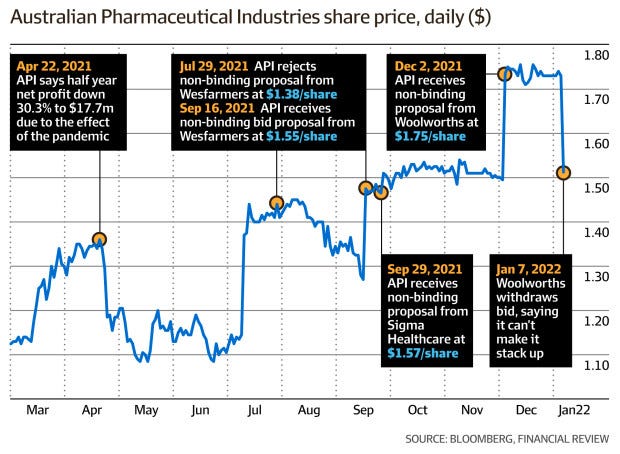

Again, a similar playbook when acquiring API 2 years back. This diagram is rather helpful:

The API situation was a different ballgame but the sequence of events are near identical. As discussed in the previous article, Woolworths withdrew due to Wes’ 20% stake rendering the crossing of the 75% threshold for a scheme of arrangement approval, a futile endeavor.

Wes returns with an offer

Wes is clearly not walking away just yet - “indicated to SILK that its due diligence investigations are ongoing.” Quite likely, Wes is banking on EC ejecting just as Woolworths did. It’s all or nothing for EC as even a partial takeout would not be viable as without full ownership, operational synergies will be difficult to implement.

But say EC decides to stick to $3.35, perhaps realizing that the price paid isn’t that hefty - a mere 9x 2023 EBITDA - then I won’t be surprised if Wes comes back with a topping bid, say ~$3.50 - maybe with the wordings “best and final” to preclude a biding war. As an antecedent, when acquiring API, Wes did raise the bid by ~12% from $1.38 to $1.55.

Perhaps, Wes decides to just leave it to EC (highly unlikely in my view, for the many reasons outlined in the previous article), then shareholders will take home $3.35.

Disclosure: Topped up

Update:

An analytical mistake I made was assuming Wes had a ~9% stake via purchased stock. This was an overlooking bias and error on my part. Wes 9% stake was contingent on the initial Process Deed being upheld, a guaranteed support by WAM which obviously revokes when a superior bid emerges (in the interest of WAM).

Thus, the fresh announcement of Wes ceasing to be a substantial holder is neither new surprise info nor a signal and should not scare traders; big picture, this prevents Wes from bullying other bidders and bear in mind, SLA is still a key strategic asset for Wes’ healthcare unit. Fingers crossed.