Pacific Current (PAC.AX) quick updates

Readers can refer to post 1 and 2 for a more thorough background on this trade but basically, PAC.AX was involved in a bidding war, multiple bidders in the fray, with the market, out of sheer inefficiency, pricing the probability of securing a binding scheme of arrangement at <50%, going to even as low as 30% throughout most of October.

Finally, on 1 Nov, after a prolonged period of gut wrenching silence, an announcement was made by PAC that GQG had offered a non-binding indicative proposal for PAC at $11 per share in cash, supported by the independent board committee (IBC) but void of approval from River Capital, PAC’s largest shareholder (17.55%). Without River, it is unlikely a scheme of arrangement can be obtained (75% vote). Regardless, GQG still “sees significant strategic merit and is exploring alternative transaction structures”, indicating they are not walking away just yet (which they could have) and willing to maneuver this impediment.

GQG’s own announcement on 2 Nov states that the $11 per share offer is an amended bid, following an initial bid on 8 September. It is worth noting two things - 1) GQG has been doing due diligence for ~3 months now, publicly affirming interest and as a corollary, is unlikely to just walk away, especially considering that 2) GQG sports a 4bn market cap and the necessary financing for PAC is something like MSD-HSD % of GQG’s market cap (i.e. small) given that 1x NAV - ~600m market cap, of which a third could be attributed to PAC’s stake in GQG - so something like ~350m of purchase financing and whatever incremental $ for a bump in the bid would be de-minimus. Let’s also not forget that 1x NAV is no longer a requirement (as above, management is supporting $11, ~90% of NAV).

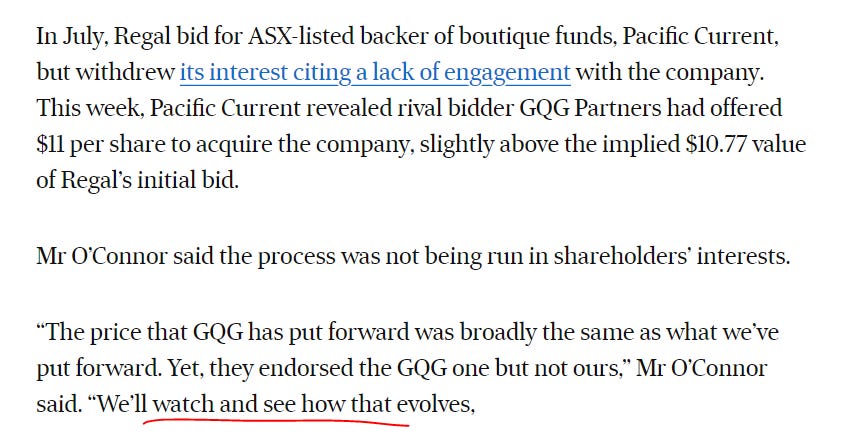

Also, let’s just circle back to the announcement for when Regal withdrew its bid - it’s quite clear, that Regal was a spurned bidder, was probably in the dark over the exact $ bid management wanted and management, to be fair, was probably engaged with other parties and trying to fish for much higher bids. Hence, it made sense for Regal to step out the ring temporarily (Regal made it explicitly clear that they’re still very interested in PAC) and let the remaining bidders battle it out to see who’s left standing before proceeding.

As per the facts above, I can draw a few conclusions

We have 2 bidders standing - Regal/River and GQG - with the likelihood of a potential bid bump by R/R as there is visibility in the process now as management has just set a price floor of $11. (positive)

We really only have those initial 2 headline bidders and every other postulated bidder has waved sayonara. (negative)

Still, the negative seems to be more or less priced into the stock. With the stock at $9.73 (last closing price) and a break of $8 and say $11 (assuming the alternative solution was GQG rolling Regal/River into a private stake for e.g.), the market is implying a mere ~60% chance of $11 turning binding. Moreover, assuming a bidding war that tops off at $11.50 per share, the market is implying ~50% probability of that happening - which seems to be way too draconian on many fronts, given the facts laid out above and also the AFR article published this morning, whereby Regal again, in the sassiest way possible, expressed dissatisfaction yet continued interest in PAC.

While the article highlights Regal purchasing another boutique i.e. PM Capital, the article also laid out that Regal still has ~ 150m of surplus capital + stock firepower - my big picture read being that Regal is very much willing to do deals as they come.

In other words, while the current spread (to $11) is pretty meh (on an absolute basis though arguably juicy IRR), I do think the market is still mispricing the dynamics here.

As to my knowledge, most following this trade would have loaded up in the low 9s given the sheer blatant mispricing then - and bear in mind (as with an earlier trade, Silk Laser) - the market panics over uncertainty (which often comes in the form of lack of communication/large shareholders exiting etc) - at 9, the downside would’ve been ~8 (a buck down) with a potential upside of 2-3 bucks and multiple bidders - yet 30% odds of a deal - atrocious inefficiency.

Let’s see how this pans.

Long PAC.AX