"Mustering" courage for Spirit (SAVE)- an update; added thoughts on bonds (8/11)

"doesn't pass muster, but if you did the following"...

I’ve discussed the SAVE arb in this post last month; there are other much more intelligent/educated writeups on the arb (free / behind paywall). David Slotnick provides solid coverage of the trial; Lionel Hutz and Jeremy Raper provide intelligent insights on the coverage points.

The stock has fallen quite a fair bit since the initial publication and I find it incredibly compelling here (I’ve ramped up the sizing); the market seems to dislike the uncertainty obviously with regards to the DoT, the proforma JBLU’s financial health and ability to pay. There’s a yoke to bear for uncertainty and while it’s not easy and light, the rewards justify.

What’s been particularly interesting about this case is the Judge’s focus on the financial health of Spirit - which is unusual - according to senior antitrust analyst Jen Rie. And this isn’t just some farce, Spirit’s senior secured notes are now trading ~70c on the dollar, implying firm distress. Before discussing the implications of this, let’s cover some key incremental pieces of info outlined in the pretrial docs and trial.

Quick Update

As usual, the DOJ in their complaints, tends to conjure a stale, lifeless and static hypothetical post-merger world failing to capture the dynamism that transpires within living, breathing and evolving business ecosystems - especially within the airline industry where planes are fungible (unlike say grocery stores) and each route, a mere dispensable cog in the national network machine, which function is to generate consolidated profits (the goal of any firm).

This is delineated in the pretrial briefs whereby the defendants argue that of the 51 overlapping nonstop routes put forth by the DOJ in 2022, 6 of them (12% HUGE) are no longer overlapping - capacity comes and goes, chasing profits. Adjusted for the contemplated divestitures, 36 of the 51 (70%) will no longer overlap, leaving the DOJ to argue that the harm on those remaining 15 routes (out of the combined 500+ routes), assuming they overlap indefinitely, would be sufficient to block a merger that is net positive on a national level.

Again, the fulcrum argument is market definition and the DOJ has historically used various market definitions to cater to their arguments - e.g. US v United Continental Holdings, a more macro market definition i.e. city competition was used rather than micro O&D route pairs. This makes sense when one considers that route level competition doesn’t occur in a vacuum - the availability of flights, time of flights - are subsets of an airline’s overall competitive strategy which governs a much larger market. If harm dealt to any trivial market (regardless of overall benefit) is enough to nullify a merger, then realistically, any horizontal merger henceforth should be rendered invalid - simply ludicrous.

The DOJ has also tried to dismiss the divestitures by arguing for an imminent replacement of competitive intensity tit-for-tat, again not acknowledging the biological-adaptation characteristics of businesses. And yes, whilst ALGT doesn’t operate the same frequency schedule as SAVE, this is not a veritable law carved governed by an eternal covenant. The ULCC subsector encapsulates dynamism-squared given their P2P networks vs the hub & spoke models operated by legacies and so shifting capacity around is a lot more straightforward. Moreover, conversion of SAVE planes to JBLU model would happen gradually (especially with the financial constraints on the pf firm) and this would provide apt time to facilitate the transition. On top of this, the residual ULCCs have order books, in aggregate, exceeding both Spirit and JetBlue combined.

In many of their arguments, the DOJ seems to put forth the SAVE of old - as if they have the financial wherewithal to grow like a weed and operate (e.g. as frequently) as before. For e.g. yeah divestments work but how about routes they do not overlap? How about future routes they could enter? These questions easily answered when one considers the viability of SAVE going forward. As mentioned, the judge seems to be paying close attention - how exactly would they continue to “disrupt” if they have to file chapter 11 imminently? And when they file, would the assets be then acquired by another airline - the scenario we find ourselves in today (OTOH could be sold piecemeal) ?

Another way of framing

Some have likened this merger situation to that of T-Mobile and Sprint

Not dissimilar to SAVE, the spread was extremely wide

This article covers the Sprint merger and provides the framework to think about the current merger situation.

In many ways, the Sprint merger had a higher hurdle, notably, the combined entity would have ~38% of the national market (vs ~8% for JBLU-SAVE) with national HHI reaching 3200 (exceeding 2500 threshold).

Merger Specificity - could both parties achieve efficiencies i.e. network growth etc. without the merger?

This was covered in yesterday’s trial and the pretrial docs but aircraft shortages (2029-2030 soonest for expected delivery of brand new Airbus order) and SAVE’s poor financial position would mean that achieving organic growth similar to the merger would be unlikely.

Merging Party is flailing

“Evidence that a merging party is a “weakened competitor” that cannot compete effectively in the future may serve to rebut a presumption that the merger would have anticompetitive effects”

As mentioned, Judge Young seems to be thinking along this lines by questioning the viability of SAVE.

Divestments

Just as the divestments to DISH (new entrant), ALGT and Frontier especially, have indicated desire to snap up those routes and expand operations. I’ve discussed this above but the revamping of SAVE aircrafts take time, providing the divestees time to integrate their operations.

Merger guidelines indicate a 2-year timeframe as reasonable time period for competitive intensity to be replaced. Frontier, in the pretrial docs, has indicated that integration can be done within 12-24 months.

Coordinated effects

Just like the mobile market, the airline market is complex/dynamic and competition involves more than just pricing (note Sorokin’s ruling for the NEA - “not just low fares but high quality service”). As mentioned above, the NEA was created because AAL couldn’t operate profitably against DAL - competition is intense, even amongst the big 4 and this merger won’t change that.

Unilateral effects

Again, it is much easier to rely on JBLU’s preceding operations as a guide rather than speculate. Moreover, reiterating again, the combined national carrier would have <10% market share.

Rehashing another old point here but the DOJ did call JBLU a maverick in the NEA trial, which “saved travelers billions of dollars”.

Other Notes

As revealed yesterday, JBLU, to fortify the argument of intentions to develop a nationwide presence (rather than eliminate a competitor like SAVE**), divulged intentions to acquire ALK prior to the pandemic of which this author argues, isn’t as sensible as an acquisition of SAVE in terms of business rationale. He also described the government’s hostility towards this merger as “bizarre” (have a read).

This is important to establish that JBLU’s intentions are pure - to compete against the big 4.

There’s quite a fair bit of debate over this statement by the judge (on the backdrop of Hayes discussing divestitures). Without knowledge of the judge’s tone, some have argued this was sarcasm though I can’t reconcile sarcasm with the subsequent “don’t read anything into this” statement.

I think Occam’s razor would imply that the judge has factored the divestitures into consideration and leans positive to approval (again I’m biased) though it’s not a sure thing just yet, his last statement - to dampen any premature excitement.

To be fair, re “don’t read anything into this” - any geezer would know this can’t be taken at face value (I’m not applying Occam’s razor here).

One question worth asking is “why’s the spread so wide? Who’s selling to me?”

I’ve been trying to source for the counter-arguments and the main contentions don’t seem to be centered on the merits of the merger (the net benefit to consumers is visible) but rather, uncertainty on the political end - congress’ love to protect the “little man against evil airline” and DoT - “if the DoT has said they’ll block it, why tango with them?”

This merger is unprecedented in nature. Firstly, there’s some “pass the bomb” at play here - SAVE standalone is in distress and post acquisition, pf JBLU will be holding the bomb and walk close to insolvency (very atypical situation). Secondly, Robin Hayes, CEO of JBLU did an interview in September indicating positive intention (“hopes JBLU wins” and a lot of integration work has been done) and some interesting facts - i) this case is very unprecedented as airline mergers have hardly been blocked and that iii) the most concentrated airport, Fort Lauderdale (mind you, Florida supports the merger), still has less than half the concentration that AAL has in Dallas/Miami and Delta in Minneapolis/Atlanta.

There are concerns that JBLU might attempt to sabotage/kill the deal especially after SAVE’s disastrous Q3. So far, JBLU has been doing a perceptibly good job but it’s also worth noting that Robin wouldn’t have been the dark about it (actually SAVE’s issues were all publicly disclosed prior) and as per the merger contract, both parties are required to use “reasonable best efforts” to close. Again, these are bindings contracts you don’t just walk away from at a whim.

Closing Thoughts

The initial downside estimation made might have been too generous given the stock touched the high 10s recently. Quite likely now, given the atrocious results and full extent of the PW engine issue SAVE faces, the stock could fall to low single digits on a break (factoring in the potential panic dump overshooting on the downside). Who exactly will be purchasing the equity then? Especially if one supports SAVE’s subtle invoking of the failing firm defense (a difficult proposition for the airline industry), then maintaining the break price at $8-$10 is plain cognitive dissonance.

On the other hand, the vanilla calls seem to have been repriced lower lately - either i) implying a lower probability of a deal close or a ii) price recut especially due to the PW engine problems - which some fear could trigger a MAC. Again MACs are generally difficult (for SAVE: A-61-62) to invoke but it’s not impossible.

Re MAC, a key line in the merger proxy: “only to the extent such developments (reference to economic/financial market changes) have, individually or in the aggregate, a disproportionate impact on the Company relative to other companies in the airline industry, in which case only the incremental disproportionate impact may be taken into account.”

The relevant industry defined is "the airline industry” so perhaps SAVE couldn’t narrow it to the ULCC market if JBLU evokes MAC. But a few points worth noting is that when the merger was orchestrated, SAVE was already heavily levered and burning gobs of cash. Even up till the trial date, JBLU upon knowledge of the fully disclosed endogenous issues at SAVE, still indicated positivity and willingness to close (see pg6 of ppt).

Though SAVE is losing more money now, the incremental impact relative to peers in its subsector is quite similar - e.g. Q3 23 EBIT (-15%) vs Q3 22 (-2.7%), is comparable to say ULCC Q3 23 EBIT (-6.1%) vs Q3 22 (6.1%) and JBLU itself Q3 23 EBIT (-6.6%) vs Q3 22 (5.4%) → similar % gap y-o-y → nothing out of pocket.

To be fair, 2) is all backward looking. Looking forward, the airline industry faces 2 endogenous headwinds - 1) overcapacity and 2) labor pressures. Scott Kirby at UAL has been very vocal about both issues, citing that due to 1), “ 2 airlines are going to account for >90% of revenue growth and pretax profitability.” In other words, a large swath of airlines will be incrementally affected. With regards, to the labor pressures, this is the “cost convergence” phenomenon Scott talks about whereby labor pressures disproportionately push up CASMX for ULCCs relative to legacy carriers. Again, this isn’t a sudden headwind - SAVE did mention outsized labor cost impacts since early last year.

SAVE is disproportionately affected by the PW engine but the issues are temporary and more importantly, they would be made whole for it.

In sum, I think the bet here is quite +ve EV. Whether it works is a separate thing but I feel the asymmetry in my gut and can’t be gun shy about it.

Added Initial Thoughts (SAVE Bonds) - 8/11/2023

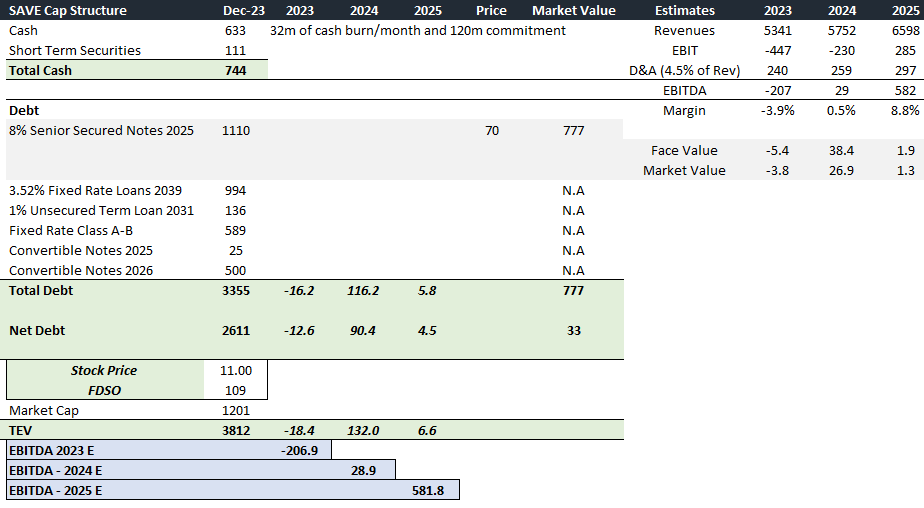

SAVE 2025 senior secured 8% notes at ~70c on the dollar appear interesting and a conservative way to play this arb. The bonds are priced for distress and stand at the very top of the capital stack.

SAVE’s liquidity profile is as follows - ~900m of liquid cash and equivalents, ~300m of untapped revolving facility and potentially ~70m break fee (assuming merger fails), incremental ~100+m and change from Gryphon as SAVE sells down the last 14 unencumbered aircrafts through 24’ + other unencumbered assets (spare engines, facilities etc).

Using street estimates on FCF, I believe SAVE burns ~30-40m of cash/month through 2024 and technically, assuming constant indefinite cash burn, SAVE would have ~2 years runway before tripping its senior note covenant - ~400m liquidity threshold. However, SAVE is also on the hook for ~120m of purchase commitments for remaining 2023 and ~450m in 2024 so the runway is a lot shorter here - ~10-12 months before SAVE trips the covenant.

Thinking through this a little, and I am no expert, assuming SAVE is able to defer some of its purchase commitments, it should be able to extend its runway out by a year or so. However, I have left out another major potential liquidity infusion event - the compensation from RTX.

The huge dump in the bond price seems to have been tied to the credit markets concern over the P&W engines; SAVE’s endogenous margin deterioration has been public information even prior to the Q3 disclosure and the only huge incremental info being the NEO engine updates (average of ~10% of SAVE’s fleet will be grounded). The market seems to be unsure of whether SAVE will *indeed* be made whole - every airline is indicating that compensation discussions are ongoing - but P&W have a reputation and franchise to maintain, they’ve doubled down on share repurchases and it would be a huge stink to the organization if they couldn’t write an adequate cheque to affected customers.

The street is estimating ~285m of EBIT in 2025 - an estimate of use to us if somehow SAVE could stem the bleeding and stay alive then, especially with the huge cheque from RTX providing cash influx to boot. As mentioned above, SAVE has been exiting certain airports i.e. cutting out unprofitable routes which should improve RASM yields, offsetting CASMX inflation. I estimate SAVE to earn ~580m of EBITDA in 2025 (8.8% margin), a far cry from pre pandemic teen margins. ULCCs used to trade at ~10x EBITDA but they’re considered inferior low margin airlines now (LMA) and I think it’s reasonable to impute a 4-5x EBITDA.

With the 8% senior notes, we are creating SAVE at a mere 1.3x EBITDA at market and 1.9x EBITDA at par, in comparison with the equity that’s going for 6.3x T+2 EBITDA.

With regards to the downside, the market is already pricing this at 30 pts off face and assuming SAVE makes it through to 2025 coupled with lower/less volatile oil prices, there’s equity like returns of 42% on capital appreciation with 2 sets of 8pts coupon clipped - not a shoddy return.

The big puzzle for me is the value of the collateral in a bankruptcy scenario - points are pretty much fungible and FWIW, Fitch estimated that the loyalty program and brand IP (of which said Senior notes are collateralized with) could be worth ~1b of value in a bankruptcy reorganization. As mentioned, it is also worth noting that SAVE had ~700m of unencumbered assets (reminder SAVE has sold down a bunch of aircrafts) in the depths of COVID - I would haircut the residual value so I’m, guessing something like ~100-200m left, covering ~ 20% of the market value of the Senior Notes now.

There are also potentially other ways to win - in a deal break scenario, Frontier might return to acquire SAVE - there’s a case for that - albeit at an equity price potentially lower than the extant price though the bonds will pan out fine (there’s quite a fair bit of equity fat between the 2 turns of leverage from net debt through EV).

Long SAVE stock, bonds, calls and JBLU calls

Hey! I couldn't find a way to contact you directly on Twitter or here. I saw you made some comments about $AVAP months ago on Twitter and, I think, also a discussion in the Lemon Fool forum. I was wondering if you had revisited this name given recent developments and your general thought about the name

Thanks for the update, very interesting. Are you playing this with options or commons?